Every Investor’s Dilemma

Risk and reward are inseparable in investing. The higher the return you chase, the more uncertainty you invite. But here’s the real question: how much risk is too much, and how much safety is too little?

I’ve seen many investors struggle with this tension. They either lock up their money in “safe” options that barely grow or gamble on high-return plays that leave them restless at night.

The truth is, balancing risk vs reward in investing is less about avoiding risk altogether and more about structuring your portfolio so your money grows in line with your goals while keeping potential losses at a level you can live with.

It involves your portfolio so that potential gains align with your financial goals while keeping possible losses at a level you can emotionally and financially withstand.

This balance is not a one-time decision but a continuous process. The sweet spot is that it let your money work for you without letting fear or greed dictate your choices.

This beginner-friendly guide walks you through exactly how to balance risk and reward in your investment portfolio, and how you can use simple tools like Sycamore NG made for Nigerian investors like you.

Why Balancing Risk and Reward Matters More Than Chasing Returns

In Nigeria, 58% of investors prefer fixed-income and low-risk products such as treasury bills, savings bonds, or fixed deposits. Most beginners enter the market with one thought in mind: how much can I make? Rarely do they ask the more important question: how much can I lose?

That mindset is dangerous because while returns may grab your attention, unmanaged risk can wipe out years of progress in one downturn.

When your portfolio isn’t balanced, you’re not only exposed to financial loss, but also to emotional strain. Investors who misjudge risk often panic when markets dip. Panic-selling turns paper losses into permanent ones, creating a cycle that sets you back instead of moving you forward.

Imagine you invest ₦500,000 into a volatile crypto asset during a bull run. In three months, it doubled to ₦1 million. You’re excited, but then the market crashes, and your holdings lose 70% overnight. Suddenly, you’re left with ₦300,000 which is far less than your starting point.

Now compare that to splitting the same ₦500,000 into safer bonds, equities, and only a fraction into crypto. The total growth would likely be smaller in the short run, but you wouldn’t be devastated by the crash.

That’s the essence of balance: it’s not about hitting jackpots; it’s about consistency. By protecting the downside, you give your portfolio the breathing room to recover and grow steadily over the long term, and that matters far more than any single lucky break.

Understanding Risk in Investments

Investment risk is the possibility that the actual outcome of your investment will differ from what you expected, usually meaning you could lose money.

Risk takes many forms, and the more you understand them, the better equipped you are to make decisions that fit your financial goals.

- Market risk: This is the most common. Prices go up and down based on economic changes, global events, or even investor sentiment. When the stock market dips, your equity holdings dip with it.

- Inflation risk: In Nigeria, where inflation has hovered above 20%, this is a huge concern. If your money is earning 5% but prices are rising at above 20%, your purchasing power is shrinking even if your balance looks bigger.

- Liquidity risk: Sometimes, you may not be able to access your money quickly without selling at a loss. For instance, trying to offload property in a downturn could force you into a bad deal.

- Default or credit risk: This happens when a borrower or bond issuer fails to pay back what they owe. Corporate bonds, for example, can carry this risk if the company runs into financial trouble.

Think about keeping all your savings in a “safe” account that earns no interest. On the surface, it feels risk-free. But over time, inflation erodes the value of every naira sitting idle. A million naira today may only buy goods worth ₦750,000 in a few years if inflation stays high. That’s a hidden risk many people overlook.

Understanding these risks doesn’t mean you avoid investing but rather it means you prepare, diversify, and choose options that protect you from being blindsided.

Understanding Reward in Investments

Reward in investing is the profit or return you expect in exchange for taking on risk. Every investment you make carries the hope of a reward. That reward can take different shapes depending on the asset:

- Steady interest income from fixed-income securities like Treasury Bills or savings bonds.

- Dividend payouts from shares in profitable companies.

- Capital appreciation, where an asset like real estate or equities grows in value over time.

- Currency protection, where holding dollars, euros, or pounds shields you from the erosion of the naira.

If you invest ₦1 million in Treasury Bills, you might earn around 13% annually with low risk. On the other hand, putting the same ₦1 million into equities could yield gains of 30% in a good year or lose just as much in a bad one. Both represent “rewards,” but the nature and predictability of those rewards differ.

Even small shifts can act as rewards. Holding $1,000 when the naira weakens from ₦1,000/$ to ₦1,400/$ instantly increases your local purchasing power by 40% without you lifting a finger.

Rewards matter because they motivate you to invest in the first place, but they only make sense when measured against the risks you’re taking. Without that balance, the promise of reward can quickly turn into disappointment.

The Risk–Reward Trade-Off: Finding the Sweet Spot

The basic rule of investing is simple: the higher the potential return, the higher the risk. You can’t remove risk entirely, but you can decide how much of it you’re comfortable carrying. That decision is what shapes your financial journey.

If you’re young, you might afford more risk because you have time to recover from downturns. A 25-year-old who invests aggressively in equities can ride out market volatility knowing they have decades ahead. But if you’re approaching retirement, your priority shifts is no longer about aggressive growth but about preserving the wealth you’ve already built.

Think of investing like driving. Speeding can get you to your destination faster, but the chance of an accident rises. Driving too slowly feels safe, but you may never arrive on time. The real key isn’t maximum speed or maximum caution but rather it is balanced. The pace that lets you arrive safely and on schedule.

That’s the essence of the risk–reward trade-off: not chasing the highest possible return, but finding the balance that aligns with your personal goals, timeline, and peace of mind.

Practical Strategies to Balance Risk and Reward

Balancing your portfolio should not be a guesswork but rather about applying practical strategies that reduce risk without killing your growth potential. Here are four approaches you can start using right away:

1. Diversify Across Asset Classes

Diversification lowers the chance that one bad bet ruins your entire portfolio. By spreading your money across equities, fixed income, real estate, and cash, you reduce the blow if one asset underperforms.

For instance, in 2009, Nigerian investors who held only Nigerian bank stocks suffered massive losses. Those who had bonds or real estate alongside equities softened the impact and recovered faster.

With Sycamore Investments, you can access diversification through Portfolio Management, where we create tailored mixes of assets based on your goals and risk appetite.

You can invest in Premium yield investment, Commercial papers, stocks, etc.

2. Match Investments to Your Goals & Time Horizon

Short-term needs require safer vehicles, while long-term goals allow for more risk.

- Saving for school fees due in a year? Treasury Bills or a Sycamore Target Savings plan fit better than volatile equities.

- Planning for retirement in 20 years? Equities or growth-focused funds can take the lead because you have time to ride out volatility.

Always ask yourself, “When will I need this money?” before choosing an asset.

3. Regularly Review and Rebalance

Markets don’t stay still. If stocks in your portfolio rise and suddenly make up 70% of your holdings (when your plan was 50%), you’re now carrying more risk than intended.

Rebalancing such as selling a portion of what’s overweight and reallocating it restores the balance.

At Sycamore Asset Management, we offer ongoing portfolio monitoring to help you keep your mix aligned with your goals without constant guesswork on your end.

4. Hedge Against Local Currency Weakness

Nigeria’s inflation and currency swings make hedging essential. Converting part of your funds into USD, EUR, or GBP can protect your wealth from naira depreciation. Holding $1,000 when the exchange rate shifts from ₦1,000/$ to ₦1,400/$ boosts your local purchasing power by 40% instantly.

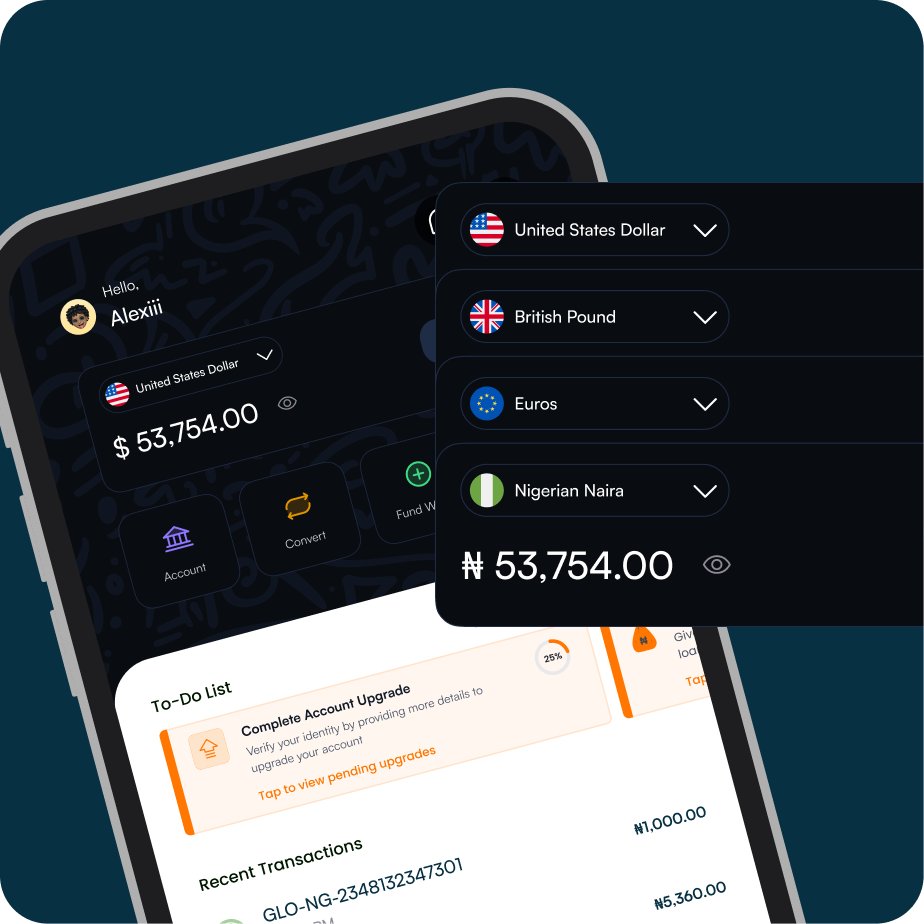

With Sycamore’s MultiCurrency (MCY), you can easily convert your money from naira into foreign currencies white still earning interest.

And if you want your dollars to grow through investment while you hold them, Sycamore’s Enhanced Dollar Investment offers interest returns above 8% per annum, allowing you to hedge and earn at the same time.

How to Set Up your Investment on Sycamore App

Step 1: Download the Sycamore app from the Play Store or App Store

Step 2: Create and verify your account. It takes less than 2 minutes.

Step 3– Fund your naira wallet (You can also convert your naira to USD for USD investment)

Step 4– Click the “Invest” button on your Sycamore app home screen

Step 5– Select either “Premium Yield Investment” , “Enhanced Dollar Investments”, Assets(Commercial papers), Stocks.

Step 6– Click “Add New Investment”

Step 7– Enter your investment name, amount( minimum of 100,000 Premium Yield Investment, $5 for Enhanced Dollar Investment,) and duration and click “Continue”

Common Mistakes Beginners Make

When you’re new to investing, it’s easy to focus on the wrong things. Here are some common pitfalls that can quietly sabotage your portfolio:

- Chasing high returns only: Jumping into speculative stocks or crypto because of hype often ends in painful losses. What looks like quick money usually comes with outsized risk.

- Over-diversifying: Spreading money across too many assets sounds smart, but it dilutes gains and makes your portfolio messy to track. Balance matters more than sheer numbers.

- Failing to rebalance: When one asset class grows faster than others, your portfolio drifts off course. Without rebalancing, you might be carrying way more risk than you intended.

- Ignoring inflation: Many people think keeping money in a savings account is “safe.” In Nigeria, where inflation eats more than 20% of value annually, that’s one of the riskiest decisions you can make.

For instance, If you leave ₦1 million in a zero-interest account for a year, you’d effectively lose about ₦250,000 worth of value to inflation. That’s money gone, not because you spent it, but because prices rose while your savings stood still.

Avoiding these mistakes doesn’t require complex strategies. It requires awareness, discipline, and a commitment to managing both sides of the risk–reward equation.

Bringing It All Together: Your Personal Risk–Reward Equation

At the end of the day, there isn’t one perfect formula for everyone. Your portfolio should reflect your goals, your age, and how much risk you can live with. What feels balanced to you may feel reckless to someone else, and that’s okay.

Balancing risk vs reward in investing isn’t about copying someone else’s strategy. It’s about finding the mix that lets you sleep at night while your money quietly works for you.

If you want tools that help you achieve that balance, whether it’s professional Portfolio Management, dollar-denominated hedges through Enhanced Dollar Investments, or steady returns from Target Savings; we at Sycamore built our platform with your peace of mind in mind.

You’ll find that balance isn’t about chasing extremes, but about creating stability that fits your life.

Click here to download the Sycamore app and start creating your stability.