The Everyday Dilemma of Choosing Where to Invest

You’ve saved ₦500,000 and you want it to grow. One friend insists you should buy stocks because “the returns are higher.” Another tells you to stick with bonds because “they’re safer.” Who’s right? That’s the everyday dilemma many investors face: stability or growth, safety or opportunity.

This decision can feel overwhelming at first, but once you grasp the basics of what each represents and how they behave in the Nigerian context you’ll see that the real power lies not in choosing one over the other, but in knowing when and how each fits into your financial journey.

Fixed income investments provide predictable, lower-risk returns, while equities offer higher growth potential but with greater volatility. The right choice depends on your financial goals and risk appetite.

In this article, we will guide you through exactly what fixed income investments and equities are, how they work, which is the best for you and how you can get started with just a little capital using simple tools like Sycamore NG that are made for Nigerian investors like you.

Breaking Down the Basics: What Fixed Income and Equities Really Mean

To make sense of the debate, you first need to understand what each option really represents. Fixed income is like giving a loan to a government or company in exchange for steady interest payments. It’s called “fixed” because you know what you’re getting upfront; it is predictable and has regular returns.

In Nigeria, examples include Treasury Bills, Federal Government Bonds, and corporate bonds. These instruments give you stability, but your upside is capped at the agreed rate.

Equities, on the other hand, are ownership. When you buy shares in a company, you’re buying a slice of that business, and with it, a slice of its profits and risks.

Your returns come from dividends (when the company pays out profits) and capital appreciation (when the share price goes up). But if the company struggles or the market turns sour, you share in the losses too.

For instance, imagine you invest ₦200,000 in a one-year FGN bond paying 15% annually. You know upfront you’ll get ₦30,000 in interest, no surprises. Now take that same ₦200,000 and put it in the stock of a Nigerian bank.

In a good year, the value could rise by 30% or fall just as much if economic policy shifts against the sector.

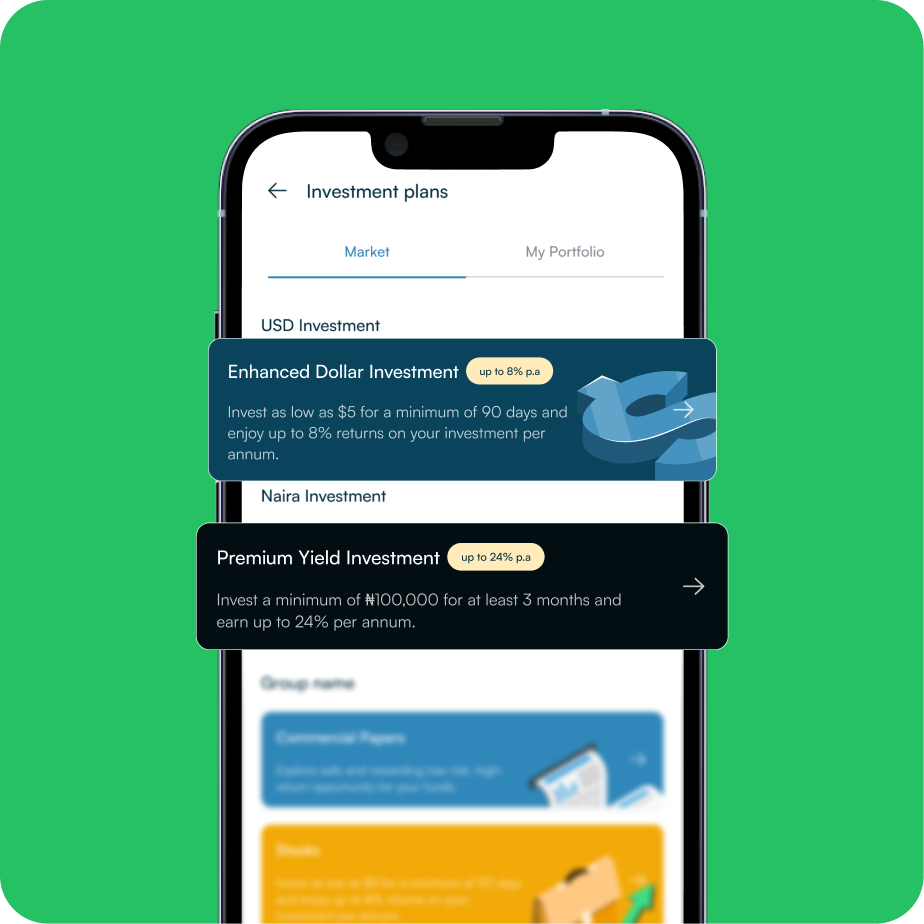

If you’re looking for higher-yield fixed income products without the hassle of picking individual bonds, Sycamore Premium Yield Naira Investment gives you access to competitive rates while still keeping your money in regulated, income-generating assets.

Both instruments play different roles, and the key isn’t deciding which is “better,” but understanding how they can work together to serve your financial goals.

How They Differ: Risk, Return, and Liquidity Compared

Equities are higher-risk, higher-reward, while fixed income is lower-risk, steadier-return.

The first difference is risk. Equities move with the market policy changes, company performance, and investor sentiment all send prices swinging. If the economy dips, your stocks can lose value overnight.

Fixed income is steadier because the terms are set in advance, but it isn’t risk-free; in Nigeria, inflation can quietly erode the “real” value of your returns.

Then there’s return. Equities have no cap because they can deliver massive growth in the right conditions, but the same volatility can wipe out part of your capital. Fixed income is capped at the interest rate you signed up for, but that predictability is often what makes it attractive.

Finally, consider liquidity: how quickly you can access your cash. Equities are usually easy to sell, though the price you get may not be favorable. Fixed income products like T-bills and bonds can lock your money until maturity, though some instruments are tradable if you need to exit early.

For instance, during the 2023 FX crisis, Nigerian equities swung wildly, bank and manufacturing stocks lost double digits in weeks. Meanwhile, Federal Government bonds kept paying steady double-digit interest. Investors who allocated part of their funds to fixed income had a buffer, while those all-in on equities felt the full impact of volatility.

Both asset types have strengths and weaknesses. The trick is matching them to your situation rather than assuming one is “always” better.

Aligning Investment Choice With Your Financial Goals

Fixed income suits short-term or safety-focused goals, while equities suit long-term growth goals.

Your decision between fixed income and equities isn’t about which one sounds better on paper but rather it’s about what you’re trying to achieve.

For short-term goals (1–3 years), safety comes first. If you’re saving for school fees, house rent, or a wedding, you can’t afford the risk of market swings. Treasury Bills, FGN Savings Bonds, or a structured savings product are more suitable.

With Sycamore Target Savings which offers up to 20% interest rate per annum, you can lock in disciplined savings at competitive rates, making it easier to hit short-term targets without surprises.

For medium-term goals (3–7 years), balance matters. A Lagos entrepreneur building a fund for business expansion could use a mix perhaps 50% fixed income for stability and 50% equities for growth. This way, you protect your capital while still positioning for upside.

For long-term goals (7+ years), equities shine. Retirement planning, wealth creation, or generational investments thrive with equities because you have time to ride out volatility. For example, investing steadily in Nigerian blue-chip stocks or even global equity funds allows compounding to work in your favor.

At the same time, pairing equities with professionally managed diversification through Sycamore Portfolio Management can give you expert guidance on keeping the right balance.

When you align your investments with your goals and timelines, the “fixed income vs equity” debate becomes less confusing. Each option has a place, and the key is choosing the right one for the job.

Inflation, Currency, and the Nigerian Reality

In Nigeria, the choice between fixed income and equities isn’t only about risk versus return. It’s about risk versus inflation and currency depreciation.

Take inflation: leaving ₦1 million in cash in 2023 meant losing above 20% of its real value. Even if your money looked the same on paper, it bought far less in the market. Fixed income offered some protection; FGN bonds at 15–17% helped cushion the blow but inflation still outpaced many returns.

Currency is another layer. When the naira weakens, the value of your local savings shrinks against global benchmarks. Equities sometimes outpace inflation, but they do so with volatility. Fixed income may lag if yields don’t keep up with rising prices. That means relying on just one category can leave you exposed.

Imagine splitting ₦1m: ₦500k into FGN bonds at 16% and ₦500k into a dollar-based investment. While inflation erodes local cash, your bonds pay predictable returns, and your dollar holdings gain value as the exchange rate rises. That dual approach not only keeps your money afloat but positions it for growth despite economic headwinds.

This is why the Sycamore Enhanced Dollar Investment was created for you. It gives you the stability of fixed income, but in USD, which helps hedge against both inflation and naira depreciation. It enables you to invest in foreign currency such as the USD for as low as $5, with up to 8% interest per annum in returns.

In the Nigerian reality, the smarter question isn’t “fixed income vs equity” but it’s how to combine them with currency hedges so your money stays relevant no matter how the economy moves.

Building a Balanced Strategy: Why It’s Not Always Either/Or

The best approach is often not choosing one over the other but blending both in proportions that fit your goals.

Equities and fixed income don’t compete but rather, they complement each other. Equities give you growth, while fixed income gives you stability. Together, they create balance.

Think of it like a seesaw: too much weight on one side tips you over. But when you spread across both, your portfolio stands firm through ups and downs.

Say you have ₦1 million and a moderate risk appetite. You could allocate it this way:

- 50% in Sycamore Premium Yield Naira Investment for high local returns.

- 30% in Sycamore Enhanced Dollar Investment to hedge against currency risk.

- 20% in carefully chosen equities for long-term growth.

This blend cushions you if equities dip, protects your wealth from naira weakness, and still leaves room for upside. Instead of asking “fixed income vs equity,” the smarter question is: what mix works best for your life right now?

Why You Should Invest in Sycamore’s Fixed Return Investment Plans

Fixed return plans give you a set return upfront over a specific period. For example, Sycamore NG offers returns of up to 24% per annum, depending on the duration and amount you invest.

- Risk level: Low to moderate, depending on the provider.

- Returns: Up to 24% annually.

- Tenure: At least 3 months.

- Minimum investment: Starts from ₦100,000 or $5(Enhanced Dollar Investment)

- How to access: Easily through Sycamore NG’s platform, with an intuitive dashboard and flexible options.

These plans are ideal if you want passive income with predictability and are ready to lock funds for a few months.

Common Mistakes Investors Make

The worst mistake is going “all-in” on one side of fixed income vs equity without considering your goals and risk appetite.

Here are a few traps many investors fall into:

- Putting all money in equities expecting quick wealth: Market swings can wipe out your capital if you don’t balance it with safer assets.

- Staying too conservative in fixed income: Parking everything in bonds or savings may feel safe, but inflation often outpaces returns, quietly eroding your wealth.

- Ignoring currency diversification: Keeping all funds in naira leaves you exposed to depreciation, especially if your future expenses are dollar-linked.

- Not reviewing their mix: Goals evolve. A strategy that worked five years ago might not fit your needs today.

During the last crypto bull run, many Nigerians shifted everything into speculative assets. When prices crashed, portfolios were devastated because nothing was set aside in bonds or dollar investments to cushion the fall.

Note that even while deciding on your allocation, you can park idle cash in a Sycamore Wallet Balance to earn daily interest instead of leaving it lifeless in a traditional account.

Mistakes don’t happen because people don’t know about investments but they happen because they don’t build balance into their decisions.

Case Scenarios: Which Investor Should Choose What?

Sometimes the best way to understand the fixed income vs equity decision is to see it play out in real lives. Here are three scenarios that show how goals, not just age, determine the right mix:

Scenario 1: The 25-year-old graduate saving for retirement

With decades ahead, time is on their side. Equities should take the lead, since short-term dips won’t derail long-term growth. A heavier tilt toward stocks, with a smaller allocation to fixed income for stability, makes sense here.

Scenario 2: The 40-year-old parent saving for children’s education

This is a medium-term goal, with a clear timeline. A balanced mix of fixed income for safety and Target Savings for discipline, plus a smaller slice of equities for growth, ensures school fees are protected while money still grows.

Scenario 3: The 55-year-old preparing for retirement in 5 years

Here, preservation trumps aggressive growth. Fixed income should dominate through bonds, T-bills, or structured products with just a light allocation to equities for modest upside. That way, retirement plans aren’t left at the mercy of market volatility.

Notice how none of these choices is absolute. The mix is shaped by when the money will be needed and what it’s meant to achieve. Goals drive allocation more than age alone.

Final Thoughts: Your Money, Your Mix

The debate over fixed income vs equity isn’t really about declaring a winner. Markets will always swing, inflation will keep testing your patience, and currencies will rise and fall. What matters is whether your portfolio is built to serve your goals, not someone else’s opinion of what’s “best.”

When you choose balance, you position yourself to grow in good times and to endure the inevitable downturns. That’s the power of aligning investments with your life’s milestones — retirement, education, business growth, or even simple wealth preservation.

At Sycamore NG, we make it easy for you to take that first step. With as little as ₦100,000, you can access our fixed return plans and start earning up to 24% per annum, without complex processes or hidden stress.