Introduction: The Fear of Losing Money Is Real

Chidi finally saved ₦1 million and, eager to grow it fast, followed a friend’s advice to jump into crypto. Two months later, his balance had shrunk to ₦400,000. What went wrong? He didn’t stop to ask the one question every beginner should: what risks am I taking?

If you’ve ever felt your stomach turn at the thought of losing money, you’re not alone. In fact, research shows that the pain of losing is psychologically twice as powerful as the joy of gaining. That fear is what makes people avoid investing altogether or dive in blindly without assessing risks first. Both approaches lead to disappointment.

This is where understanding risk becomes your best ally. Rather than seeing it as something to run from, you can measure it, manage it, and even use it to your advantage.

You can assess investment risk in Nigeria by looking at potential losses, time horizon, and the stability of each investment option, then balancing them against your goals.

And here’s the good news: assessing risk isn’t as complicated as it sounds with using the right platform like Sycamore NG.

What Risk Really Means in Investing

When most people think of risk, they picture losing money. But in investing, risk is much broader because it’s the uncertainty of outcomes. Sometimes that uncertainty works in your favor with higher returns; other times it erodes your capital. Understanding the different types of risk helps you see where the real threats lie.

There’s market risk, which comes from price fluctuations. Stocks, crypto, even some bonds can swing wildly, and if you need to sell during a downturn, you lock in losses. Then there’s inflation risk: returns that don’t keep up with rising prices. This is especially real in Nigeria, where inflation sits above 20%. An investment yielding 10% may look fine on paper, but in real terms, you’re actually losing money.

Another layer is liquidity risk of which the danger of not being able to access your funds when you need them. Think of real estate: property values often rise over time, but if you suddenly need cash, you can’t sell a house overnight. Finally, credit risk applies to fixed-income products. If a borrower or issuer defaults, you may never see your principal back.

For instance: Treasury bills carry very low credit risk because they’re backed by the government. But they do carry inflation risk because if the yield is 15% and inflation is above 20%, your real value is shrinking. Real estate, on the other hand, protects well against inflation since property values generally rise, but it carries high liquidity risk because you can’t quickly convert land into cash in an emergency.

Risk isn’t a single monster; it’s a mix of moving parts. Once you see them clearly, you can plan how to keep them in check.

Defining Your Risk Tolerance

Your first job as an investor is to know yourself. Risk tolerance is simply how much loss you can stomach without panicking. If your portfolio drops by 30% tomorrow, will you calmly hold on or will you cash out in fear? Your honest answer determines what kind of investments you should even consider.

Several factors shape this tolerance. Your age matters: the younger you are, the more time you have to recover from dips, so you can generally afford higher-risk assets. Income stability plays a role too. A salaried worker with steady pay can take more risks than a freelancer with unpredictable earnings.

Dependents matter because if your kids’ school fees depend on that cash, your tolerance is naturally lower. And then there’s personality: some people thrive on volatility; others lose sleep over a 5% dip.

“Your risk tolerance is how much loss you can stomach without panicking.”

Here’s a practical tool to gauge yourself: ask two simple questions. One, “If my investment drops by 30%, can I sleep at night?” Two, “Do I need this money in less than a year?” Honest answers give you a baseline. If you said “no” to the first or “yes” to the second, you’re on the conservative side.

For example, a 30-year-old with a stable ₦500k monthly salary and no dependents may be fine riding short-term dips for long-term gains. A retiree relying on savings for daily expenses, however, should prioritize low-volatility options to preserve capital.

Knowing your risk tolerance is like knowing your driving speed. Some roads allow 120 km/h, but if you’re only comfortable at 80, forcing yourself faster could cause a crash.

Matching Risk with Time Horizon

Even if you’re comfortable with risk, the timing of when you’ll need your money should dictate how much risk you actually take. The shorter the time horizon, the less room you have for market fluctuations to “smooth out.” That’s why short-term funds must stay in safer, more predictable places.

Money you’ll need in less than a year has no business being in volatile assets. If you’re saving ₦2 million for rent due next year, parking it in stocks or crypto is reckless. One downturn could derail your plans.

Instead, keep it in instruments like treasury bills, fixed deposits, or Sycamore Investment (Premium Yield Naira Investment or Dollar Enhanced Investment), where growth is steady and predictable.

For medium-term goals (one to three years), a balanced approach works better. You might combine real estate savings schemes, managed portfolios, or diversified naira and dollar investments. These options protect your funds while still giving them a chance to grow.

For long-term goals (five years or more), you can take on higher volatility because time is your friend. Equities, real estate, and dollar-denominated investments become suitable. Even if prices dip temporarily, years of compounding usually bring you out ahead.

If you’re planning for a house purchase in 10 years, equities or a diversified portfolio make sense. But if you’re setting aside ₦500k for your child’s school fees next term, a short-term, low-risk instrument is the only safe route.

The golden rule? Match your risk level to how soon you’ll need the money. Time can heal market swings, but only if you give it enough runway.

Diversifying Your Portfolio

According to a report, diversified portfolios reduce volatility by up to 30% compared to non-diversified ones. If there’s one principle every investor should memorize, it’s this: don’t put all your eggs in one basket.

Diversification spreads your money across different assets so that one bad outcome doesn’t sink your entire portfolio. Diversification spreads your eggs across baskets so one bad outcome doesn’t wipe you out.

There are several ways to diversify. You can mix asset classes such as splitting between naira fixed-income securities, FX-denominated assets, stocks, and real estate. You can diversify within industries.

For instance, holding shares in both a telecom company and a bank, instead of concentrating everything in one sector. And you can spread across currencies, hedging part of your wealth in dollars while the rest stays in naira.

For instance: Let’s say you have ₦5 million. A reasonable allocation could be ₦2 million in fixed-income instruments, ₦1.5 million in dollar assets, ₦1 million in stocks, and ₦500k as a cash buffer. If one asset class underperforms, the others cushion the blow.

At Sycamore, diversification is built into our Portfolio Management service. Experts help you design a mix that fits your goals and tolerance, investment planning, asset acquisition advisory, corporate investment advisory, and market and investment advisory, ensuring your idle funds aren’t overexposed to a single risk. This way, your portfolio can grow steadily while minimizing unpleasant surprises.

Think of diversification like a football team. You wouldn’t put 11 strikers on the field—you need defenders, midfielders, and a goalkeeper. Each plays a role, and together they give you the best chance of winning. Your investments should work the same way.

Use Simple Risk Metrics (Beginner-Friendly)

You don’t need to be a CFA charterholder to understand whether an investment carries too much risk. A few simple checks can tell you a lot about what you’re getting into.

Start with Maximum Drawdown; this looks at the biggest drop an asset has experienced in the past. If a stock once fell 70% in a year, you should be prepared for the possibility it could happen again. Then consider Historical Volatility: how much do prices typically swing from month to month? If they bounce around wildly, that’s a red flag if you’re risk-averse.

Another easy metric is the Inflation Benchmark. Ask yourself: is this investment beating Nigeria’s above 20% inflation rate? If not, you might be growing on paper but losing in reality.

For instance: An investment yielding 12% annually may sound impressive at first. But when inflation is above 20%, you’re effectively losing above 8% of purchasing power each year. That’s like filling a bucket with water while it leaks from the bottom, and you’ll never get ahead.

As a beginner, these simple filters are enough to keep you grounded. If you know how much an investment can drop, how wild the swings are, and whether the returns beat inflation, you’re already ahead of most first-time investors who jump in blind.

Manage and Reduce Risk

Assessing risk is only half the job. The other half is actively managing it so you don’t expose yourself to unnecessary losses. A few basic rules can save you from the mistakes that wipe out many beginners.

1. Never invest money you can’t afford to lose

If the funds are meant for rent, medical bills, or daily expenses, they don’t belong in volatile assets.

2. Always research the provider

Is the platform SEC-licensed? Are they transparent about where your money goes? Regulation is your first line of defense against scams.

3. Avoiding concentration

Don’t put 80% of your wealth into a single investment, no matter how “promising” it looks. Spread it out, so one bad bet doesn’t drag you down.

4. Set up automated rules for yourself

For example, decide in advance to sell an asset if it falls by 20%. That way, emotions don’t dictate your decisions when prices swing.

For instance, someone who was lured into a scheme promising “30% monthly returns” ends up losing their entire ₦1 million when it collapses in MMM-style fashion.

By contrast, keeping that money in regulated options like Sycamore Investments not only earns steady returns but also removes the risk of waking up to find the platform has vanished. You can invest in:

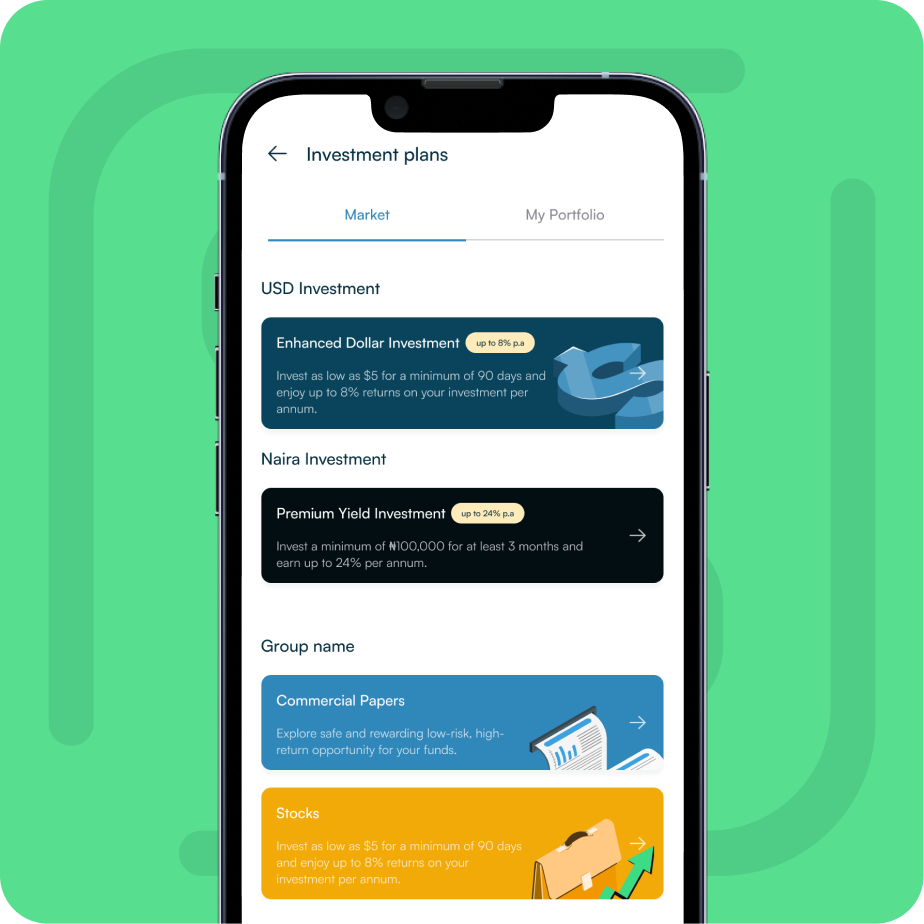

1. Premium yield investment: Minimum of 100,000 Premium for at least 3 months and earn up to 24% per annum.

2. Enhanced Dollar Investment: Where you can invest as low as $5 for a minimum of 90 days and enjoy up to 8% returns on your investment per annum. You just convert your naira from your wallet into USD, euros, or pounds ahead of time

3. Assets: You can explore safe and rewarding low-risk, high-return opportunities such as, commercial papers, Treasury bills, stocks, savings bonds, FGN bonds, corporate bonds, and eurobonds, etc.

At Sycamore, we deliberately filter investment opportunities so you don’t have to worry about Ponzi traps. By sticking with regulated, transparent channels, you reduce the odds of catastrophic loss while still keeping your money productive.

“Risk will always exist, but how you manage it determines whether it becomes a pothole or a cliff.”

Mistakes Beginners Make

When you’re just starting out, it’s easy to trip over the same mistakes many others have made. The good news? By spotting them early, you can sidestep costly lessons.

- Copying friends without doing your own research: Just because someone close to you invested in crypto, land, or a “sure deal” doesn’t mean it fits your goals or tolerance. What works for them may ruin your peace of mind.

- Ignoring inflation: You may feel satisfied earning 8–10% annually, but with inflation around 25%, your real wealth is shrinking. A ₦1m account balance looks stable after five years, but in reality, it has lost over ₦500k in purchasing power.

- Confusing saving with investing: Parking money in a current account may feel safe, but it’s not investing, it’s erosion in disguise. True investing means putting money where it grows beyond inflation, even if gradually.

- Being aware of “guaranteed” high returns: Any scheme that promises 30% monthly is not an investment but it’s a Ponzi dressed up as one. The crash is only a matter of time.

Someone saving ₦1m in a current account for five years might believe they’re being disciplined. But after half a decade of inflation, that “safe” ₦1m has lost nearly half its value in real terms.

In contrast, channeling the same money into regulated vehicles like Sycamore Premium Yield Naira would have preserved and grown its worth.

By avoiding these beginner traps, you save yourself years of regret and set the foundation for smarter, steadier investing.

How to Diversify your Portfolio Investment on Sycamore App as a Beginner

Step 1: Download the Sycamore app from the Play Store or App Store.

Step 2: Create and verify your account. It takes less than 2 minutes.

Step 3– Fund your Naira wallet (You can also convert your naira to USD for USD investment)

Step 4– Click the “Invest” button on your Sycamore app home screen

Step 5-Select either “Premium Yield Investment” , “Enhanced Dollar Investments”, Assets (Commercial papers,), Stocks.

Step 6– Click “Add New Investment”

Step 7– Enter your investment name, amount (minimum of 100,000 Premium Yield Investment, $5 for Enhanced Dollar Investment,) and duration and click “Continue”.

Closing: Risk Can Be Managed, Not Eliminated

The truth about investing is that risk never disappears, rather you can only learn to live with it wisely. The goal isn’t to chase “risk-free” returns (they don’t exist) but to take smart risks that match your goals, your time horizon, and your comfort level. When you do that, your money grows while you sleep easier.

Think of risk management as the line between gambling and investing. Gamblers throw money at chances they don’t understand, hoping luck stays on their side. Investors study the risks, diversify, and align their moves with long-term plans. That discipline is what builds wealth over time.

And when you’re ready for practical tools to put this into action, Sycamore offers beginner-friendly options like Investments, and Portfolio Management to help you invest smarter from day one.