You don’t need to be rich or even “financially savvy” to take control of your investments.

Thanks to mobile apps, simplified investment platforms, and tools tailored to the Nigerian market, more people are skipping traditional consultants and building their own investment plans.

The best part is that you can do this without feeling overwhelmed or needing to become a finance expert. In Nigeria, usage of investment apps grew by more than 200% between 2021 and 2024 (Data from NIBSS & App Annie).

You can build a custom investment plan without a financial advisor, defining your financial goals, know your cash flow and tolerance risk, Create a Simple Budget That Prioritizes Investing, Choose the Right Investment Channels Based on Your Goals, etc.

This guide shows you how to build a self-guided investment plan, step by step, using real logic, simple systems, and digital platforms like Sycamore that are built for people like you.

Step One: Define Your Financial Goals Clearly

The first and most important step in building an investment plan without an advisor is understanding why you’re investing.

Without clear goals, you’re just guessing. That’s where many first-time, self-guided investors go wrong, and they throw money into “what’s trending” without linking it to a specific outcome.

But when your goals are defined, it becomes easier to choose the right investment tools, manage your risk, and measure success.

Think about what you want your money to achieve.

- Do you want to pay your rent in six months?

- Are you saving for a laptop, a car, or your child’s school fees?

- Maybe you’re planning a relocation, retirement, or starting a business?

Whatever it is, write it down. Don’t just keep it in your head.

Now, sort each goal into one of these categories:

- Short-term goals (0–12 months): e.g. travel, emergency fund, rent

- Medium-term goals (1–3 years): e.g. car purchase, postgrad, down payment

- Long-term goals (3+ years): e.g. home ownership, retirement, children’s education

Assign a timeline and a price tag to each goal. For instance:

- “Buy a new laptop in 6 months – ₦350,000”

- “Pay annual rent in 11 months – ₦800,000”

- “Relocate in 2.5 years – ₦4 million”

Once you’ve done this, you’ll have a map. And from here on, every investment decision you make will have a direction—because you’ll know exactly what you’re working toward.

Step Two: Know Your Cash Flow and Risk Tolerance

Before you commit a single naira to any investment, understand how much you can actually afford to invest, and how much risk you can live with.

Many people either overestimate how much they can invest or throw in all their savings without considering emergencies. On the flip side, some people let fear hold them back completely.

The key is finding the balance between your cash flow (what you have left after essential expenses) and your risk tolerance (how much uncertainty you’re comfortable with).

1.Calculate Your Investable Income

Start by tracking your monthly income and expenses. It doesn’t have to be fancy, just write down:

- Total income (e.g., salary, freelance, side gigs)

- Fixed expenses (e.g., rent, food, transport, bills)

- What’s left = your potential investment amount

Let’s say you earn ₦250,000 monthly:

- Rent + food + bills = ₦180,000

- You have ₦70,000 left.

Out of that, maybe ₦30,000 is realistic to invest monthly.

2. Assess Your Risk Tolerance

Ask yourself:

- Can I handle fluctuations in value?

- Will I panic if I see losses?

- Do I want fixed returns, or am I okay waiting longer for possible higher gains?

If you’re unsure, try free online risk tolerance quizzes (Google: “risk tolerance questionnaire Nigeria” or use tools on sites like Investopedia).

Low Risk = you want safety and stability → consider FGN Bonds, Money Market Funds, or Sycamore’s Fixed Income Plans

Medium Risk = you’re okay with some ups and downs → add Balanced Funds, Multi-currency wallets, or Real estate micro-investments

High Risk = you can wait for long-term gains and tolerate losses → explore Equity Funds, Crowdfunding, or Commercial Papers

Step Three: Create a Simple Budget That Prioritizes Investing

A solid budget isn’t just about controlling your spending but your tool for funding your future.

As a self-guided investor, budgeting creates the discipline to invest consistently, no matter your income level.

Without structure, even the best investment plan can fall apart. You might “intend” to invest ₦20,000 monthly, but without a budget and automation, it’s easy to spend it on other things.

Budgeting gives your money direction and helps you treat investing like a monthly necessity, not an afterthought.

1. Use a Simple Budgeting Framework

You don’t need anything complicated. One of the easiest methods is the 50-30-20 rule:

- 50% for Needs (rent, bills, food)

- 30% for Wants (entertainment, dining out)

- 20% for Savings & Investments

So, if you earn ₦300,000 monthly:

- ₦150,000 goes to essentials

- ₦90,000 for wants

- ₦60,000 is available for investing or saving

You can also flip this rule if you want to be aggressive: make it 40-30-30 or even 50-20-30, with 30% going into investments. The key is consistency over perfection.

2. Automate Your Investments

Manual investing is hard to sustain. You might forget, delay, or second-guess your decisions.

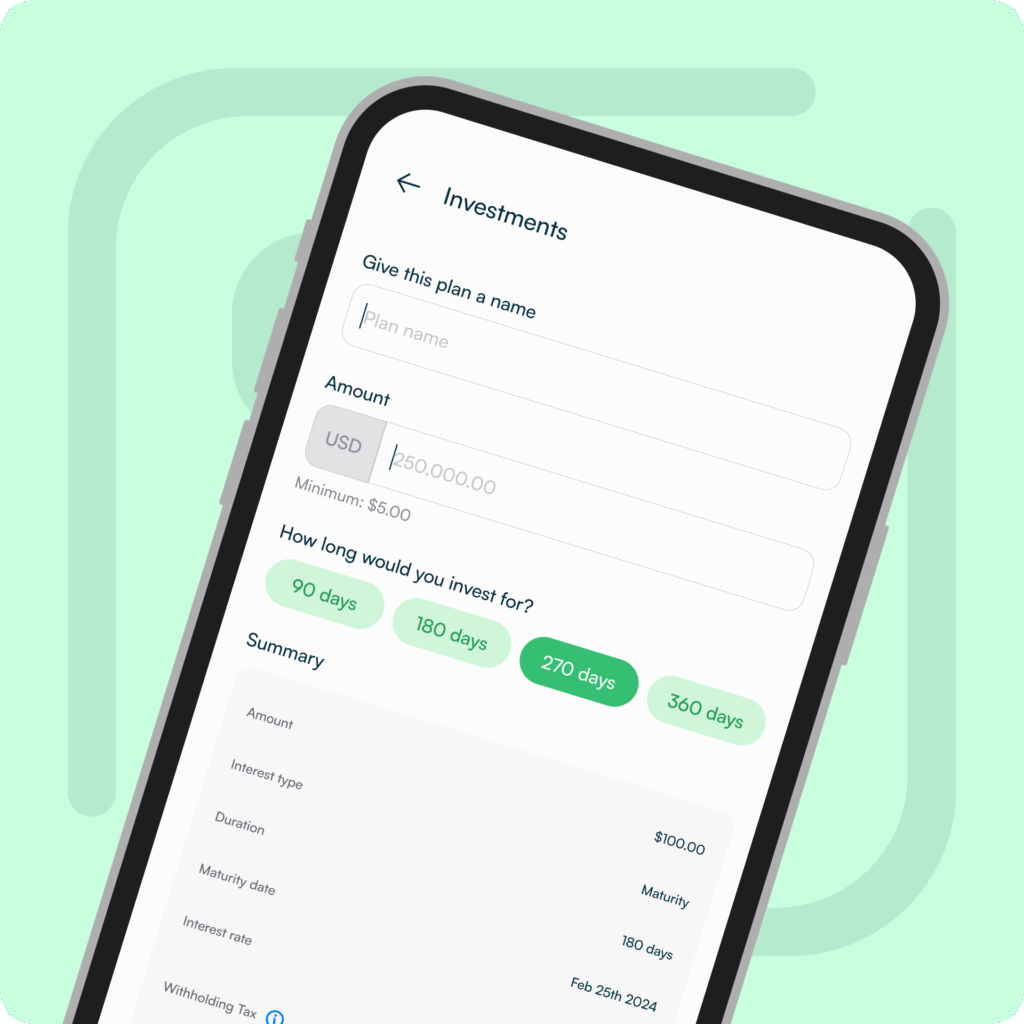

With Sycamore’s Target Savings, you can set automated weekly or monthly contributions toward a goal, and earn 3% cashback on your bills just for staying consistent.

3. Set Visual Reminders

Budgeting works best when your goals stay top-of-mind. Write down your goal on a sticky note. Name your bank savings account after the goal (e.g., “Laptop Fund” or “Canada Plan”).

Seeing your reason regularly helps you stick to your budget and sacrifice today for tomorrow’s gain.

Step Four: Choose the Right Investment Channels Based on Your Goals

Every investment tool has a purpose, and the right choice depends on how soon you’ll need the money.

If you’re saving for rent in 6 months, locking that money in a 3-year bond would be a mistake. Likewise, putting your retirement savings in a high-risk equity fund meant for short-term trades could backfire.

Matching your goals with the right investment channel keeps your plan realistic and effective.

Let’s break this down based on timelines with examples and suggested tools for each.

1 . For Short-Term Goals (0–12 months)

Think: rent, travel, emergency fund, laptop purchase. Best tools:

- Money Market Mutual Funds – Low risk, yields around 12–18% p.a., access funds within 24–48 hours.

- Treasury Bills – Sold via commercial banks or brokers, 91–364 days maturity, government-backed.

- Sycamore Fixed Income Plans – Short tenors (as low as 90 days), returns up to 27.5% per annum depending on tenor and capital size.

For instance, If you need ₦300,000 in 10 months to pay your rent, investing ₦30,000 monthly into a money market fund or Sycamore’s 3-month plan ensures you build up capital while earning interest, without risking access.

2. For Medium-Term Goals (1–3 years)

Think: business capital, school fees, relocation, car purchase. Best tools:

- FGN Savings Bonds – Offered monthly, start from ₦5,000, backed by government, fixed rates 13–17% p.a.

- Multi-currency Wallets – Protects against naira depreciation. Sycamore’s USD Wallet helps hedge with easy access.

- Real Estate Micro-Investment Platforms – Like FundREIT or Brickstone; invest in fractional property ownership or rental income pools.

3. For Long-Term Goals (3+ years)

Think: retirement, home purchase, children’s education. Best tools:

- Balanced Mutual Funds or Equity Funds – Higher long-term returns (15–25%+), but with more short-term risk.

- Corporate Bonds or Commercial Papers – Offered by companies, vetted fintechs like Sycamore; higher yield but do your due diligence.

- Crowdfunding Projects – AgriTech or infrastructure crowdfunding (e.g., FarmCrowdy, Treepz) with long-term ROI potential.

Step Five: Diversify and Balance Your Investment Portfolio

Even without a financial advisor, you can, and should diversify your investments to manage risk and improve your overall returns.

Diversification simply means spreading your money across different types of investments so you’re not overly dependent on one outcome.

If one investment underperforms, others may pick up the slack. It’s one of the most important personal finance strategies Nigerians can adopt, especially in an economy where inflation, currency fluctuations, and market shocks are common.

1. A Simple Diversification Strategy

You don’t need to invest in 10 different platforms or juggle complex asset classes. Start with this 3-way breakdown:

- 40% in safe, fixed-income investments: E.g., Sycamore’s Fixed Income Plan, FGN Bonds, Treasury Bills. These give you stability and predictable returns.

- 30% in liquid funds for easy access: E.g., money market mutual funds, USD wallets, or Sycamore’s daily-interest wallet. These act as your emergency or “just-in-case” buffer.

- 30% in long-term growth options: E.g., equity mutual funds, micro real estate, or high-yield corporate bonds. These can provide higher returns, but may require more patience.

2. Why This Matters

When you’re investing without an advisor, balance is your best protection.

- You won’t panic if one product underperforms

- You always have some money accessible

- You steadily build wealth over time, even in a volatile market

And with platforms like Sycamore offering both fixed income and flexible savings tools, you don’t need multiple accounts to build a well-rounded portfolio. It’s all about finding the mix that aligns with your income, timeline, and confidence level.

Step Six: Track, Reassess, and Adjust Regularly

Your investment plan isn’t a “set it and forget it” document. To stay relevant to your life, it needs regular check-ins and updates. Life changes. Maybe you land a better-paying job. Or maybe a goal becomes more urgent, like relocating sooner than planned.

Without reviewing your plan periodically, you risk misalignment between your current needs and your original strategy. Even self-guided investors need a feedback loop.

1. Revisit Every 3–6 Months

Ask yourself:

- Are my financial goals still the same? Has something shifted? Are you saving for a baby now? Did you cancel a relocation plan?

- Has my income improved or declined? A raise, a lost gig, or new expenses can change how much you can invest—or where to focus.

- Do any investments need rebalancing? Maybe your money market fund is now 60% of your portfolio because it performed well. Time to reallocate and restore balance.

This step keeps your plan alive, relevant, and optimised, not just reactive.

2. Tools to Track Your Investment Plan

You don’t need fancy software to monitor your progress. Start with:

- Google Sheets or Excel: Create a simple tracker with your monthly contributions, expected returns, and goal timelines.

- Budgeting apps like Money Lover or Rise can also track goals and savings.

- Sycamore’s dashboard: Lets you view your fixed-income products, wallet balances, and target contributions all in one place, helping you see real growth over time.

The Sycamore app puts your portfolio in your pocket. Download it today to track your progress in real time and stay in control.

Story Snapshot: How Yemi Built Her First Investment Plan Alone

At 29, Yemi, a freelance designer living in Lagos, had no clue where to start with investing. She wasn’t earning a fortune but just around ₦250,000 a month, but she had a dream to buy a new laptop for work, save for her rent due in 10 months, and start building long-term savings. She didn’t have an advisor. Just a ₦150,000 buffer and a little curiosity.

Here’s what she did: she put ₦100,000 into a Sycamore Fixed Income Plan for 90 days to earn passive interest, and Saved ₦50,000 in her USD wallet on Sycamore to hedge against naira depreciation

Within 6 months, she earned returns from her fixed income, gained confidence, and reinvested the profits without consulting anyone. More importantly, she understood her investments. She chose tools that matched her goals. And she kept things simple and trackable.

Like Yemi, you can start small and grow with confidence. Download the Sycamore app now and begin your journey today.

Common Mistakes to Avoid in Self-Guided Investing

Managing your own investment plan gives you freedom, but that freedom comes with responsibility. Avoiding common missteps is key to protecting your money and peace of mind.

The common mistakes to avoid in self-guided investing are copying twitter or TikTok trends without context, locking up all your funds in long-term products, Ignoring Inflation When Calculating Returns, etc.

1. Copying Twitter or TikTok Trends Without Context

Just because someone on social media made ₦500k in 3 weeks doesn’t mean the same approach fits your goals or risk appetite. Many influencers push aggressive investment ideas without disclaimers. If you don’t understand the tool or the strategy, don’t copy it.

2. Locking Up All Your Funds in Long-Term Products

Yes, long-term tools can offer great returns—but what if you need cash for rent or emergencies? Without access to liquid investments like money market funds or Sycamore’s daily-interest wallet, you might end up borrowing just to solve urgent needs.

3. Ignoring Inflation When Calculating Returns

If your investment gives 8% annual return while inflation is 28%, your money is actually shrinking in real value. Always ask: Is this return above the inflation rate? That’s why tools like Sycamore Fixed Income Plans (up to 27.5% p.a.) or multi-currency savings can help hedge against local value loss.

4. Choosing Unregulated Platforms

Any app or site that offers quick returns with no clear license, partner institution, or accountability structure is a risk. Only use platforms registered with SEC Nigeria or backed by credible partners. Sycamore, for instance, provides full transparency and is locally regulated.

5. Overdiversifying into 10+ Tools You Can’t Track

Trying too many investments at once can backfire. If you can’t monitor them all, you may miss early warning signs or fail to reinvest your returns. A better approach: choose 2–4 tools you understand well and stick to them. Simplicity wins.

Conclusion: Invest Confidently Without an Advisor

You don’t need a financial advisor to take control of your future. You just need clarity, discipline, and the right tools.

Whether you’re earning ₦70,000 or ₦700,000 a month, you can build a practical investment plan that reflects your goals. And you’re not alone.

Platforms like Sycamore NG were built for everyday Nigerians who want to grow their money safely and smartly.

From high-yield fixed income plans to USD wallets and automated savings tools, you have everything you need to execute your plan, without needing to hire a consultant.

Your money deserves a mission. Start now. Your future self will thank you.

Download the Sycamore app here and put your investment plan into action